Your car gets repaired after an accident and may look perfect. But when you try to sell or trade it in, buyers often offer less or walk away entirely because the accident now appears on the vehicle history report.

That difference between what your car was worth before the crash and what it is worth now is called diminished value. Under California law, you may be able to recover that loss from the at-fault driver’s insurance company.

Most drivers never file this claim because insurers rarely mention it. This guide explains what a California diminished value claim is, who qualifies, how it is calculated, and how to recover the compensation you may be owed.

What Is a California Diminished Value Claim?

A California diminished value claim is a legal demand for compensation for the permanent reduction in your vehicle’s resale market value caused by an accident that was someone else’s fault. The claim is made against the at-fault driver’s liability insurance, not your own insurance policy.

California courts have long recognized diminished value as a compensable form of property damage. The legal principle is straightforward: when another person’s negligence damages your property, they are responsible for the full extent of that damage, including the loss in value that remains even after the vehicle has been fully repaired.

Third-party claimants in California have the right to pursue diminished value as part of an auto property damage claim. The reasoning is simple. Two identical vehicles, one with a clean history and one with a reported accident, will not sell for the same price. That difference represents a real financial loss, and California law allows you to recover it.

There is one important limitation. In most cases, you cannot file a diminished value claim against your own collision coverage if you were at fault for the accident. Instead, the claim must be pursued as a third-party claim against the at-fault driver’s insurer.

| Important: Insurance Companies Will Not Tell You About This Under California law, an insurer is not required to volunteer that you have the right to file a diminished value claim. If you do not know to ask for it, they will not bring it up. You must initiate this claim yourself or work with a qualified car accident attorney who will. |

The Three Types of Diminished Value

California auto property damage law recognizes three distinct types of vehicle value loss. Understanding which type applies to your situation determines how your claim is built and what evidence you need.

| Type | When It Applies | What It Measures |

|---|---|---|

| Inherent Diminished Value | After full repair. This is the most common claim type | The permanent market stigma from having an accident on the vehicle history report, regardless of repair quality |

| Repair-Related Diminished Value | After repairs that failed to fully restore the vehicle | Extra value loss caused by repairs, mismatched paint, non-OEM parts, or unresolved structural issues |

| Immediate Diminished Value | Before repairs are made. This is rare | The difference between the pre-accident and post-accident value before any repair work is done |

Inherent diminished value is by far the most common basis for a California diminished value claim. It requires no proof of bad repairs; the accident history alone on a Carfax or AutoCheck report is sufficient to demonstrate the loss. Even well-repaired vehicles with accident histories fetch measurably lower prices than comparable clean-history vehicles in every market segment.

Repair-related diminished value applies when the repairs themselves were substandard, such as mismatched paint, non-OEM replacement parts, improperly aligned panels, or unresolved structural issues. This type of claim stacks on top of inherent diminished value and often requires a certified appraiser to document the repair deficiencies.

Who Can File a Claim in California?

You are eligible to file a California diminished value claim if all of the following conditions are true:

- Another driver was at fault (or primarily at fault) for the accident that damaged your vehicle

- Your vehicle sustained damage that reduced its market value, even if fully repaired

- Your vehicle was still worth something prior to the accident (high-mileage vehicles with pre-existing significant damage have reduced claim potential)

- You are filing within three years of the date of the accident under California’s statute of limitations for property damage

- You are filing as a third-party claimant against the at-fault driver’s insurance, not against your own policy

California also allows diminished value claims under Uninsured Motorist Property Damage (UMPD) coverage of up to $3,500 in cases where the at-fault driver is identified, but only if you carry that optional coverage and the driver was actually identified. Hit-and-run situations may not be covered under UMPD in California.

Comparative negligence applies in California. If you were 20% at fault for the accident, your recoverable diminished value is reduced by 20%. You can still pursue a claim even with partial fault, your compensation is simply adjusted proportionally under California’s pure comparative negligence rules.

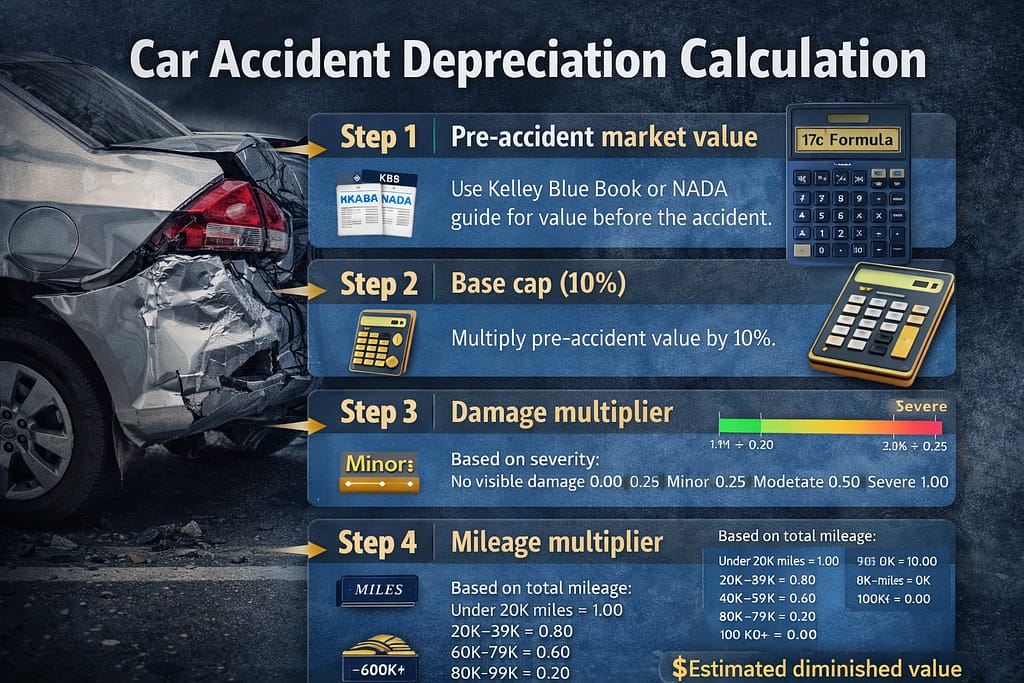

How Car Accident Depreciation Can Be Calculated: The 17c Formula

The insurance industry’s standard method for calculating inherent diminished value is called the 17c Formula, named after section 17c of a Georgia Supreme Court ruling that became industry-wide standard practice. It is a three-step formula, and understanding it is critical because insurers consistently manipulate it to minimize payouts.

| Step | Variable | Description |

|---|---|---|

| Step 1 | Pre-accident market value | Use Kelley Blue Book or NADA for your vehicle’s fair market value on the date of the accident |

| Step 2 | Base cap (10%) | Multiply pre-accident value by 10% to get the maximum starting figure, e.g., $30,000 vehicle = $3,000 cap |

| Step 3 | Damage multiplier (0.00–1.00) | Severe structural damage = 1.00. Major = 0.75. Moderate = 0.50. Minor = 0.25. No visible damage = 0.00 |

| Step 4 | Mileage multiplier (0.00–1.00) | Under 20K miles = 1.00. 20K-39K = 0.80. 40K-59K = 0.60. 60K-79K = 0.40. 80K-99K = 0.20. 100K+ = 0.00 |

| Result | Estimated diminished value | Example: $3,000 x 0.50 (moderate) x 0.60 (42,000 miles) = $900 insurance estimate |

Why the 17c Formula Often Undervalues Your Claim

The 17c formula is a starting point, not a ceiling. Insurance adjusters frequently manipulate it by assigning artificially low damage multipliers, arguing the vehicle falls into a lower mileage bracket, or misrepresenting the pre-accident market value. A 2024 Kelley Blue Book report documented a real case where KBB’s own editor filed a claim expecting a settlement of $650 to $715 based on the formula and the insurer offered only $400, with no clear explanation of the calculation used.

This is why independent appraisals matter. A certified professional appraiser using market analysis tools, including vAuto market data, NADA archival valuations, and Carfax, produces a more accurate and harder-to-dispute figure than the 17c formula alone. When negotiating with an insurer, a certified appraisal report carries significantly more weight than the insurer’s own internal estimate.

| Real-World Example A 2022 Toyota Camry worth $28,000 before the accident. After repair, it is worth $24,500, a $3,500 loss. Under the 17c formula with moderate damage (0.50) and 38,000 miles (0.80): $28,000 x 10% = $2,800 cap. $2,800 x 0.50 = $1,400. $1,400 x 0.80 = $1,120 insurer estimate. An independent appraiser using market comparables puts the actual loss at $3,500. The difference is $2,380; money the insurer will pocket if you accept the formula-based offer without challenge. |

Why Insurance Companies Lowball Diminished Value Claims

Car accident depreciation claims are among the most undervalued insurance payouts in the country, and that is not an accident. Insurers have a financial incentive to minimize or deny these claims, and they use several predictable tactics to do it:

- Claiming the vehicle was “adequately repaired.” Adjusters argue that because the vehicle was returned to its pre-accident mechanical condition, no diminished value exists. California law explicitly rejects this argument; the market stigma from accident history creates real, measurable value loss regardless of repair quality.

- Using the 17c formula against you. By assigning the lowest possible damage multiplier and mileage modifier, the formula produces a minimal payout figure that the adjuster can point to as “calculated” rather than arbitrary.

- Offering a quick, lowball settlement. As documented by SnapClaim and other appraisal services, insurers frequently make a first offer that is a fraction of the actual loss, hoping the claimant will accept it without pushback. Accepting any settlement check may constitute a waiver of further claims.

- Delaying the claim. Prolonged delays wear down claimants. While the three-year statute of limitations gives you time, evidence degrades and market comparables shift.

- Disputing fault allocation. Even where fault is clear, adjusters may assign partial blame to the claimant to reduce the payout under California’s comparative negligence rules.

| Do Not Cash That First Check Without Reading the Fine Print Insurance companies sometimes embed release language in settlement checks or accompanying letters. Cashing a check that contains release language can legally terminate your right to pursue additional compensation, including your full diminished value. Have an attorney review any settlement documentation before you sign or cash anything. |

Step-by-Step: How to File a California Auto Property Damage Claim

Filing a California auto property damage claim for diminished value requires more than just calling the at-fault insurer and asking for money. Here is the process that produces results:

- Wait until repairs are fully complete. Diminished value is most accurately calculated and hardest to dispute after the vehicle has been professionally repaired. The gap between the pre-accident market value and the current post-repair market value becomes concrete and documentable.

- Establish the pre-accident market value. Use Kelley Blue Book, NADA Guides, or an independent appraisal to document your vehicle’s value on the date of the accident. Save the output. This is your baseline figure.

- Obtain a professional diminished value appraisal. An independent, certified appraiser who specializes in California auto property damage claims will produce a written report with market comparables, vehicle history analysis, and a documented loss figure. This report is your primary negotiating tool.

- Submit a written demand letter. Send a formal demand to the at-fault driver’s insurer that includes the appraisal report, the accident report, repair documentation, and your calculated diminished value figure. Put everything in writing. Verbal requests are easily denied or ignored.

- Negotiate and do not accept the first offer. The first settlement offer from an insurer is almost always below the actual loss. Counter with your certified appraisal. If the insurer refuses to negotiate in good faith, the next step is either small claims court (up to $12,500, no attorney representation allowed in California small claims) or a formal lawsuit.

- Escalate to litigation if necessary. If your claim is denied or the insurer offers an inadequate settlement and refuses to negotiate, you can file a lawsuit directly against the at-fault driver within the three-year statute of limitations. A California auto property damage attorney can handle negotiations and litigation, and fees are often contingency-based for diminished value claims that also involve personal injury.

Diminished Value vs. Total Loss: What Is the Difference?

These two concepts address different situations, and understanding the distinction matters for your California auto property damage claim:

Diminished value applies when your vehicle is repaired but is now worth less due to its accident history. You retain ownership, and the car is drivable, but its market value has permanently dropped.

Total loss occurs when the cost to repair the vehicle exceeds a threshold of its pre-accident actual cash value (ACV). In California, when the repair cost surpasses approximately 75–80% of ACV, the insurer typically declares the car a total loss and pays out the ACV rather than repair costs. Once a vehicle is declared a total loss, you do not file a diminished value claim; the total loss settlement replaces it.

If you believe your vehicle’s ACV was calculated too low in a total loss determination, you can dispute the valuation with the insurer or request an independent appraisal. The process of contesting a total loss ACV is a separate claim type from a diminished value claim, though both fall under California auto property damage law.

It is also worth noting that if your vehicle has a recurring manufacturer defect unrelated to the accident, say a transmission issue or electrical failure, you may have overlapping rights under the California lemon law, which operates independently of any accident-related property damage claim. The key changes to California lemon law in 2025 under AB 1755 have also introduced new filing deadlines worth knowing if you have a concurrent manufacturer defect claim.

California Diminished Value Claims in Glendale

Los Angeles County consistently ranks among the highest in the state for vehicle accident frequency, with heavy traffic corridors like the Ventura Freeway (134), Interstate 5, and State Route 2 running through Glendale. Vehicle collisions are common throughout the city.

The congested freeway corridors and surface street density mean that Glendale vehicle owners face an above-average risk of post-accident value loss.

Despite this, the vast majority of Glendale drivers who suffer property damage in accidents caused by others never file a California diminished value claim. Insurers operating in the Glendale and broader LA market rely on this. A qualified local attorney can make the difference between walking away from a lowball offer and recovering the full value of what you lost.

If you are a vehicle owner in Glendale dealing with a diminished value claim, a disputed California auto property damage settlement, or related vehicle rights questions, a consultation with a lemon law firm in Glendale, CA that also handles auto property damage claims gives you a single point of contact for the full range of vehicle-related legal rights.

Frequently Asked Questions for Diminished Value Claims

How much can I recover from a California diminished value claim?

It depends on your vehicle’s pre-accident value, the severity of the damage, and the quality of repairs. A vehicle that loses 10% to 30% of its value is typical, with losses as high as 50% possible for heavily damaged vehicles. A $30,000 vehicle could yield a claim anywhere from $900 (using the insurer’s 17c formula on a mild claim) to $6,000 or more based on a certified appraisal.

How long do I have to file a California diminished value claim?

Three years from the date of the accident under California’s statute of limitations for property damage. However, waiting erodes your evidence base and makes market comparables harder to establish. File as soon as repairs are complete.

Can I file against my own insurance?

Generally no, if you were at fault. First-party claims against your own collision coverage for diminished value are not recoverable in California. You must file a third-party claim against the at-fault driver’s insurer. The exception can bef you have Uninsured Motorist Property Damage (UMPD) coverage and the at-fault driver was uninsured and identified.

Do I need an attorney to file a California diminished value claim?

For smaller claims under $12,500, the California small claims court is an option and attorneys are not permitted. For larger claims or when the insurer disputes fault or value aggressively, an attorney is strongly recommended. Because many auto property damage attorneys work on contingency for cases that also involve personal injury, a free consultation is a low-risk starting point.

Does the accident need to be reported to file a diminished value claim?

In most situations. You can make a police report or accident report as foundational documentation for your claim. If law enforcement did not respond to the accident, file an SR-1 report with the California DMV within 10 days if the damage exceeded $1,000 or there were injuries.

Can I still sell my car after filing a diminished value claim?

Yes. Filing the claim and receiving compensation does not require you to keep the vehicle. The value loss occurs the moment the accident appears on your vehicle history report, and you are entitled to be compensated for that loss immediately — regardless of whether you sell the car or keep it for ten more years.

Not Sure If You Have a Claim? Get a Free Consultation.

If your vehicle lost value after an accident, you may be entitled to compensation that insurers rarely offer voluntarily.

A qualified California auto property damage attorney can review your situation, evaluate your vehicle’s diminished value, and help you pursue the compensation you deserve.